CBAM uncertainty shadows Europe’s urea and nitrogen markets

Uncertainty is rife through Europe’s nitrogen and urea markets as the EU’s Carbon Border Adjustment Mechanism (CBAM) gets closer to enforcement on 1 January 2026.

Importers, producers and traders are struggling to decipher the implication of a tax that remains vague, with additional costs expected anywhere from €30-80/t on imports.

CBAM reporting begins on 1 January 2026, but the actual financial liability will only be known in 2027, which is a cause of concern for importers. ‘We are liable if the producer misreports emissions, but there is no verification system in place. It is a huge risk,’ an importer said.

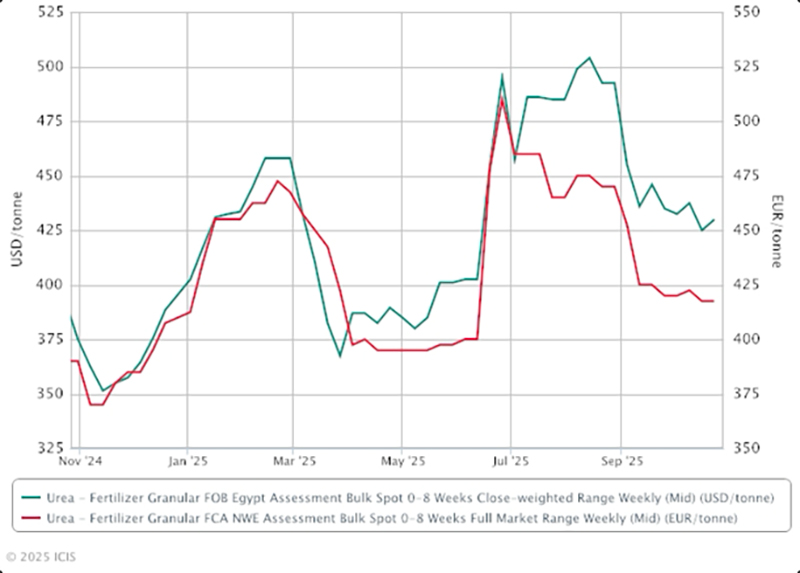

The fear of penalties, which could be based on default values as high as €140/t in France, has already triggered panic buying, especially after a French webinar miscommunicated the scope of default values. Buyers are rushing to secure November loadings that can clear customs before CBAM kicks in on 1 January 2026, which has seen Egyptian values jump by $30/tonne in a few days.

‘Anything that clears customs before the 1 January deadline avoids CBAM. People want product to reach latest two weeks before end December, so it clears customs in time,’ said a trader.

Producers in Egypt are concerned about the CBAM implications and are expected to move more product to non-European destinations in 2026 as Europe would no longer be a premium market.

Some Egyptian producers such as El-Nasr Company for Intermediate Chemicals (NCIC) and Egyptian Chemical Industries (KIMA) may benefit as they are newer plants and would have lower emissions. The overall competitiveness of Egyptian urea is however expected to decline in Europe.

European producers are also concerned. While CBAM is designed to bring fair competition with foreign suppliers, their free carbon allowances under the EU emissions trading scheme (ETS) are being phased out through 2034.

‘Costs will rise even for us. We will pay more as allowances shrink,’ said a major producer.

Philippe Rombaut, owner of Bulgarian fertilizer producer Agropolychim has criticized CBAM, warning it will drive up costs for both the fertilizer industry and European farmers. Rombaut argues that that farmers may struggle to compete with imports from countries not facing similar carbon costs, especially when selling grains to non-EU markets where buyers would not pay extra for low-carbon products.

The market is bracing for a busy November followed by a subdued H2 December-January. ‘No one will buy in January (2026). There will be port activity, but no export movement,’ said another trader.

Granular urea prices in Egypt have jumped as traders begin securing cargoes, but European values are yet to increase in the same quantum as end users still have stocks. Seasonal buying will pick up in the next few weeks.

The complexity surrounding CBAM will not only reshape trade flows but also trading behaviour, with only registered entities that can handle CBAM formalities expected to do business in Europe.

‘This will clear out occasional traders. Only serious players will remain,’ said a local trader.

The biggest impact will be the reduction in imports into Europe, with buyers again relying on domestic production. Domestic producers are already ramping up, and buyers are bound to shift to nitrates including calcium ammonium nitrate (CAN), ammonium nitrate (AN) and urea ammonium nitrate (UAN) to make up for any urea shortfall.

‘Europe doesn’t need to import. They can buy truckloads locally when they need it,’ said the trader.

Import dependency is expected to reduce but not entirely go away, especially in the peak season. Current annual urea capacity in Europe is estimated at 6.4mln t with operating rates were around 75%, while imports in 2024 are believed to be around 8.8mln t.

As the season begins, importers are rushing to secure product before CBAM reshapes trade, but with limited storage, high prices, and regulatory ambiguity, the nitrogen market is entering uncharted territory.